On May 20, 2020, the Office of the Comptroller of the Currency (OCC) adopted a final rule intended to modernize the agency’s regulations under the Community Reinvestment Act (CRA). The proposed rule was jointly released on December 12, 2019 by the OCC and Federal Deposit Insurance Corporation (FDIC), but the FDIC declined to join the OCC’s final rulemaking. As a result, the final rule only applies to national banks and federal savings associations, which the OCC indicates account for the majority of CRA activity in the U.S. The final rule makes changes in four areas of the current CRA framework:

- Clarifies and expands the lending, investment, and services that qualify for CRA consideration.

- Updates how banks delineate the assessment areas in which they are evaluated.

- Provides additional methods for evaluating CRA performance consistently and objectively.

- Requires reporting that is timely and transparent.

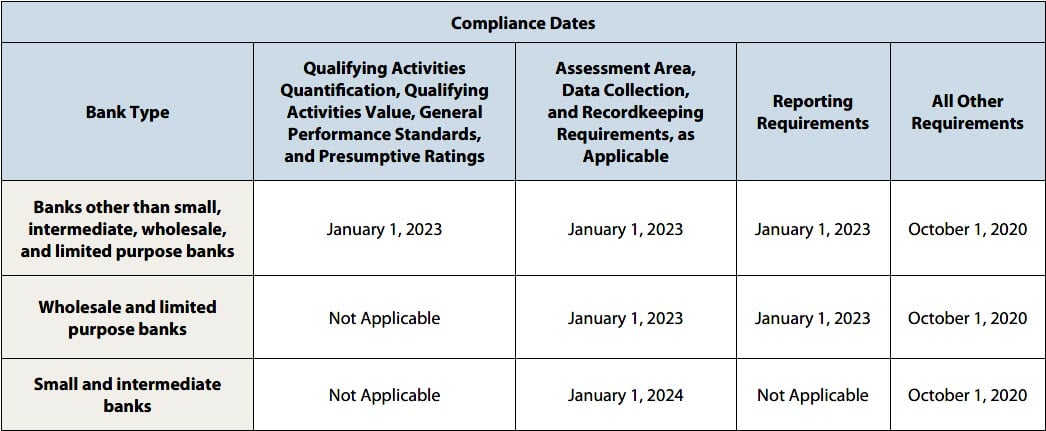

The final rule is effective October 1, 2020, but most banks will have until January 1, 2023 to comply with the final rule. Between October 1, 2020 and a bank’s new compliance date, the bank may either comply with existing CRA regulations in effect as of September 30, 2020, or may voluntarily comply with the new amended regulations. The OCC provided the following chart detailing the compliance dates and the application of the specific rule sections:

Clarification and Expansion of Activities That Qualify for CRA Credit

The final rule defines a “qualifying activity” as an activity that helps meet the credit needs of a bank’s entire community, including low- and moderate-income (LMI) individuals and communities, economically disadvantaged individuals and entities, LMI census tracts, and other identified areas of need. Activities that are on a bank’s balance sheet as of the final rule’s effective date (other than home mortgage loans or consumer loans provided to middle- or upper-income individuals in LMI census tracts) will still qualify for CRA credit under the new framework. However, the final rule provides credit only for activities that a bank undertakes directly, and not by any affiliates.

Qualifying retail loans include loans provided to an LMI individual (regardless of residency), loans to a CRA-eligible business or farm, retail loans provided in Indian country or other tribal and native lands, and small loans (up to $1.6 million) to any business or farm in an LMI census tract. The final rule includes consumer loans provided to LMI individuals and in Indian country or other tribal or native lands in the qualifying criteria but removes credit cards and overdraft products from the definition of a “consumer loan.” Further, retail loans in LMI areas to non-LMI borrowers will no longer receive CRA credit.

Qualifying community development (CD) loans, CD investments, and CD services include financing or supporting: (1) rental housing likely to be inhabited by LMI individuals; (2) another bank’s CD activities; (3) community support services such as childcare, education, or workforce development programs that partially or primarily serve LMI individuals or families; (4) economic development for small businesses, small farms, or other targeted areas of need; (5) essential community facilities or infrastructure that primarily benefit LMI individuals, LMI census tracts, or other targeted areas of need; (6) certain family farm transactions and support; (7) federal, state, local, or tribal government programs that serve LMI individuals, LMI census tracts, or other targeted areas of need; (8) financial literacy programs for individuals of all income levels; (9) housing development in Indian country or other tribal and native lands; (10) qualified opportunity funds that benefit LMI qualified opportunity zones; and (11) other activities, including capital investments and loan participations, by a bank in cooperation with a minority depository institution, women’s depository institution, Community Development Financial Institution (CDFI), or low-income credit union.

The final rule increases the threshold for qualifying loans to a small business or small farm to $1.6 million (from $1 million for loans to small businesses and $500,000 for loans to small farms). Further, CD services are no longer required to be related to the provision of financial services, but may include volunteer hours and manual labor provided to a CD project. Under the current regulation, banks receive credit for the pro rata share of a loan or investment in certain mixed-income housing. However, the final rule gives pro rata credit to all CD activities that provide some benefit to specified populations, entities, or areas. For example, a bank would receive credit for 40 percent of the dollar value of a grant that supports a nonprofit organization that provides aftercare and activities to a school where 40 percent of the students are eligible for free or reduced-price school lunches.

The OCC also published a CRA Illustrative List of qualifying activities that will be updated annually in response to requests for confirmation that an activity qualifies. Individuals may request that the OCC confirm an activity is a qualifying activity by submitting a request form to be available on the OCC website.

Delineation of Assessment Areas

The current framework defines assessment areas solely on where a bank has branches and deposit-accepting ATMs. However, this does not account for Internet banking or other banking models that collect significant portions of their deposits outside these geographic areas, resulting in a misalignment problem. Under the final rule, the scope of a bank’s assessment area is determined by two tests:

- Facility-Based Assessment Area: Every bank must delineate an assessment area encompassing each location where it maintains its main office, a branch, or a non-branch deposit-taking facility that is not an ATM, as well as the surrounding locations where the bank has originated or purchased a substantial portion of its qualifying retail loans. Notably, a bank may include deposit-accepting ATMs when delineating its assessment areas.

- Deposit-Based Assessment Area: A bank that receives 50 percent or more of its retail domestic deposits from outside its facility-based assessment area must delineate separate, non-overlapping assessment areas in the smallest geographic area where it receives 5 percent or more of its retail domestic deposits, based on the physical address of the depositor.

The OCC defines “retail domestic deposits” as the deposits of individuals, partnerships, and corporations reported in the Call Report as RCE, item 1. In addition, the final rule clarifies that retail domestic deposits also include (1) non-brokered reciprocal deposits that are sent to, but not received by, other institutions; (2) listed deposits; and (3) municipal deposits. Banks may exclude prepaid card funding, HSA deposits, sweep deposits, and brokered deposits from their retail domestic deposits. The final rule also permits a bank to change its assessment area delineations once a year.

Methods for Evaluating CRA Performance

Valuation of qualifying activities

Under the final rule, the next step in measuring a bank’s CRA performance after determining the appropriate assessment areas is calculating the value of its qualifying activities, both in the aggregate and on an assessment area basis. In each case, the qualifying activity value is calculated as:

Additionally, to incentivize certain activities or address situations where an activity may be undervalued using the balance sheet method, the final rule applies the following two times multipliers to the quantified value of certain activities:

- Activities provided to or that support minority depository institutions, women’s depository institutions, CDFIs, and low-income credit unions, except activities related to mortgage-backed securities.

- CD investments, except CD investments in mortgage-backed securities and municipal bonds.

- CD services.

- Affordable-housing-related CD loans.

- Retail loans generated by branches in LMI census tracts.

- Qualifying activities in “CRA deserts” (as defined by the OCC).

These qualifying activities may also receive a four times multiplier depending on the OCC’s determination of the activity’s responsiveness, innovativeness, or complexity.

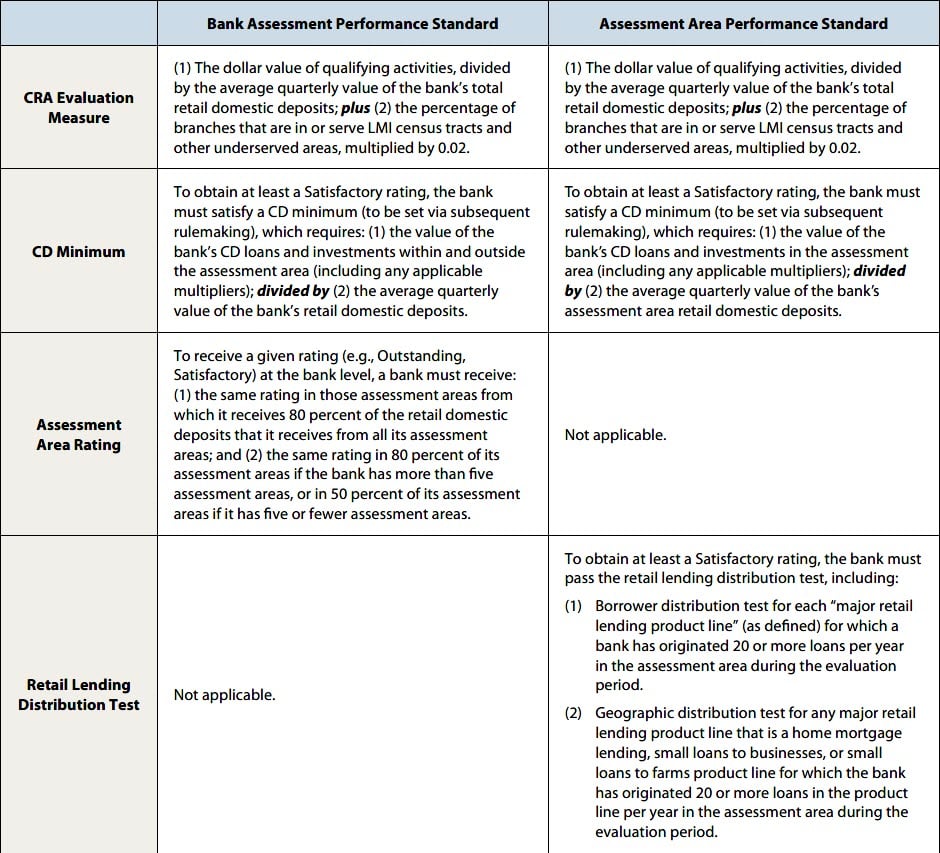

General performance standards and presumptive rating

The current framework includes a qualitative and quantitative assessment of the dollar value and number of CRA activities, but it does not set a threshold for the total dollar volume of a bank’s CRA activities in evaluating CRA performance, nor does it provide a uniform method for assessing a bank’s capacity and opportunity to meet CRA performance standards. The final rule, however, establishes new presumptive ratings applicable to the bank and assessment area performance standards. These ratings are “presumptive” because the OCC may adjust the ratings upward or downward based on various performance context factors such as: (1) the bank’s product offerings and business strategy; (2) the assessment area needs and opportunities; (3) financial condition or safety and soundness considerations; (4) innovativeness, complexity, and flexibility of the bank’s qualifying activities; (5) the bank’s competitive environment, as demonstrated by peer performance; and (6) any other information deemed relevant by the OCC. Any discriminatory or other illegal credit practices will also negatively affect a bank’s rating. The OCC intends to issue additional guidance to promote consistent application of the performance context factors.

In the final rule, banks with greater than $2.5 billion in assets are subject to the general performance standards. Small banks (those with $600 million or less in assets), intermediate small banks (those with more than $600 million, but not more than $2.5 billion in assets), and wholesale and limited purpose banks can opt into the general performance standards.

Importantly, the final rule does not set the numerical thresholds used in its new general performance standards required to obtain an “Outstanding” or “Satisfactory” rating under the CRA evaluation measure, the CD minimum, or the percentages needed to pass the retail lending distribution test. Such threshold amounts will be determined by the OCC’s subsequent rulemaking. Below is the framework of the presumptive ratings under the general performance standard:

Under the borrower distribution test, the percentage of the bank’s loans in a given category in the assessment area that the bank has made to LMI individuals, small businesses, or small farms (as applicable) must meet or exceed a demographic or “peer comparator,” which is based on a percentage of either: (1) families or households in the assessment area that are LMI, or businesses or farms in the assessment area that are small businesses or small farms (as applicable); or (2) peer banks’ loans within the category in the assessment area that the peer banks have made to LMI families, households, small businesses, or small farms (as applicable).

Under the geographic distribution test, the percentage of the bank’s home mortgage loans or small loans to businesses or farms in the assessment area that the bank has made in LMI census tracts must meet or exceed a demographic or “peer comparator,” which is based on the percentage of: (1) owner-occupied housing units, businesses, or farms in the assessment area that are in LMI census tracts; or (2) peer banks’ home mortgage loans, loans to businesses, or loans to farms in the assessment area that peer banks have made in LMI census tracts.

The final rule does not specify the length of an evaluation period, and the OCC will continue its current practice of publishing evaluation schedules to provide sufficient clarity and flexibility. However, the OCC expects that evaluation periods will be between three to five years in length.

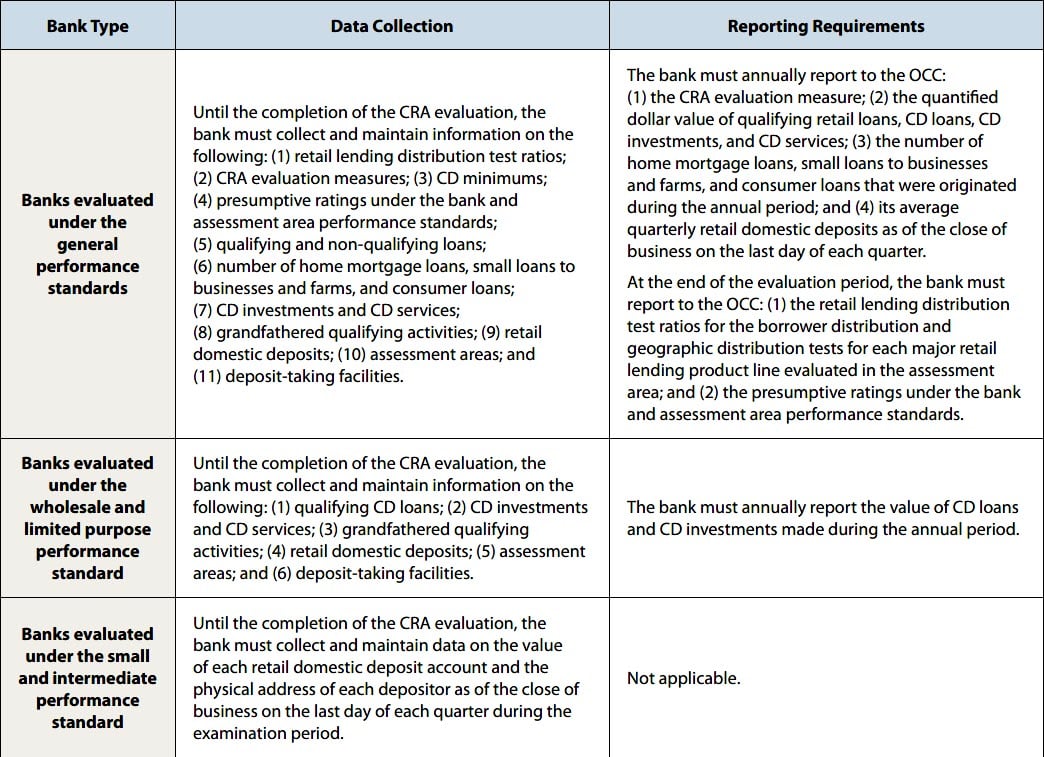

Data Collection, Recordkeeping, and Reporting Requirements

The recordkeeping and reporting requirements in the final rule are intended to produce more standardized CRA performance evaluations in less time than the current framework. The final rule imposes additional data collection and reporting requirements on banks that the OCC acknowledges will be costly to implement. The OCC, however, expects that the long-term benefits will outweigh the costs. An overview of the data collection and reporting requirements applicable to banks under the final rule is provided below:

Final Thoughts

The OCC’s analysis of the current framework found a weak positive relationship between ratings and actual CRA lending. The OCC’s new rule is a significant step forward in modernizing and clarifying CRA assessments for many banks, replacing the three tests of the existing CRA regime—the lending test, investment test, and deposit test—with a new system that seeks to couple objective, quantifiable, and transparent measures with the flexibility to adjust performance targets based on “performance context.” The rule is designed to provide incentives to achieve performance goals, as opposed to the current practice of “grading on a curve” relative to peers. However, the result is complicated and will require banks regulated by the OCC to completely reevaluate their CRA compliance and reporting programs in the coming years.

Additionally, there is still significant uncertainty about the implementation of the new rule. The OCC omitted several key numeric thresholds in the general performance standards, which will necessitate further rulemaking. The OCC also faces political headwinds, with members of Congress and community groups openly objecting to the rule, and Joseph Otting, the Comptroller of the Currency who championed the initiative to revamp the CRA framework, has resigned. As a result, the rule could still change significantly over the course of the phase-in period.

If the FDIC and Federal Reserve do not adopt the OCC’s final rule, then different CRA regimes will apply to banks that are not regulated by the OCC, which could potentially disrupt some CRA-driven initiatives that rely on collective participation by multiple banks. Further, OCC ratings under the new rules can impact other applications and authority not administered by the OCC, such as bank holding company acquisition proposals and other applications.