As we previously summarized, on April 9, 2020, the Federal Reserve announced it would purchase up to $600 billion in participations in eligible loans through the Main Street Lending Program as part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act via the Main Street New Loan Facility and the Main Street Expanded Loan Facility.

After receiving more than 2,200 comment letters on the program, many of which critiqued the universe of eligible lenders and eligible borrowers as too small to accomplish the stated purpose of the program to provide liquidity to small and medium-sized U.S. businesses in light of COVID-19-related disruptions, the Federal Reserve released on April 30, 2020 a revised Main Street Lending Program that expanded and further clarified the scope of eligibility, as well as added a third loan option—the Main Street Priority Loan Facility.

The most notable of the revisions to the program include:

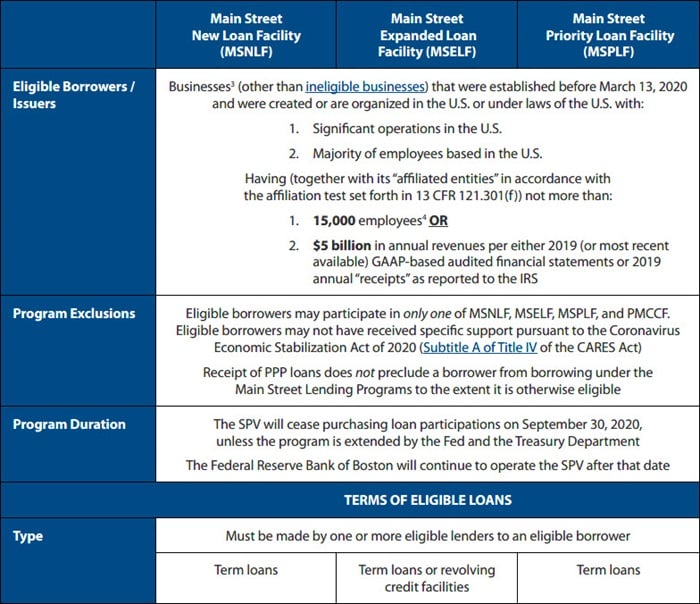

- Significant changes to borrower eligibility standards (increasing the maximum employee count from 10,000 to 15,000 and increasing the maximum annual revenue limit from $2.5 billion to $5 billion, while also announcing that the SBA affiliation rules otherwise applicable to the SBA Paycheck Protection Program (PPP) under the CARES Act apply when calculating these limitations).

- Expansion of the group of lenders eligible to participate in the program to include U.S. subsidiaries and branches of foreign banks (though still excluding private credit lenders).

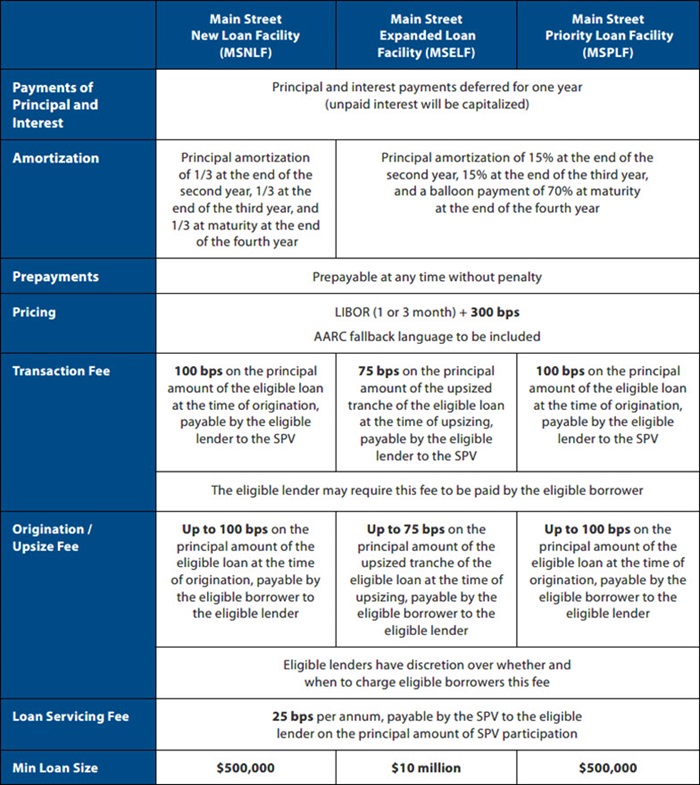

- Release of detailed amortization schedules for each program following the 12-month payment holiday.

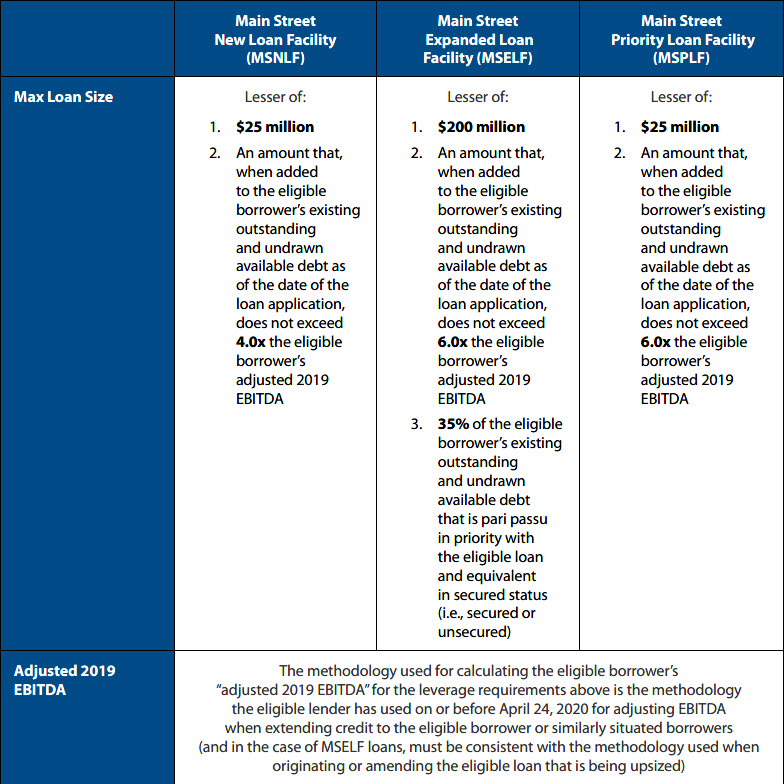

- Expansion and clarification of the methodology for calculating adjusted EBITDA for purposes of calculating the leverage limitations under each of the loan facilities.

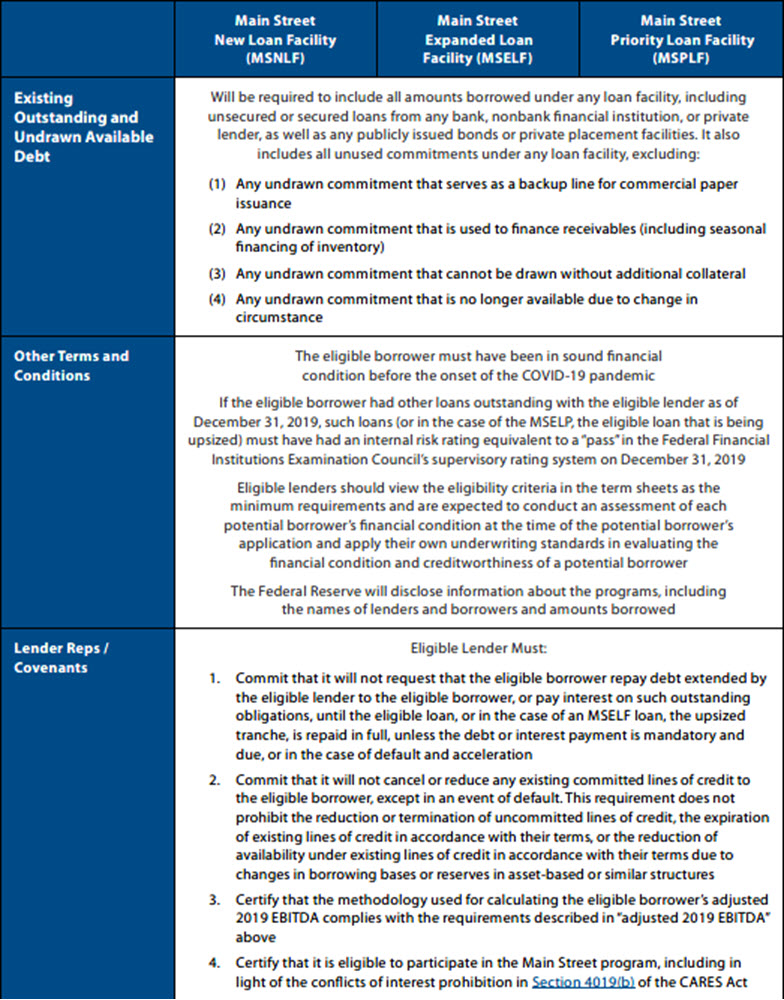

- Clarification that only the upsizing lender under the Main Street Expanded Loan Facility must satisfy the “eligible lender” criteria. To the extent the underlying facility is a multilender facility, the failure of all lenders to meet the eligible lender criteria does not preclude the loan from being upsized under this program.

- Clarification that the requirements set forth in the Main Street Lending Program term sheets are only a floor to borrower eligibility and that eligible lenders are expected to apply their own underwriting standards when evaluating the financial condition and creditworthiness of a potential borrower before determining whether they are approved to receive a loan under the program.

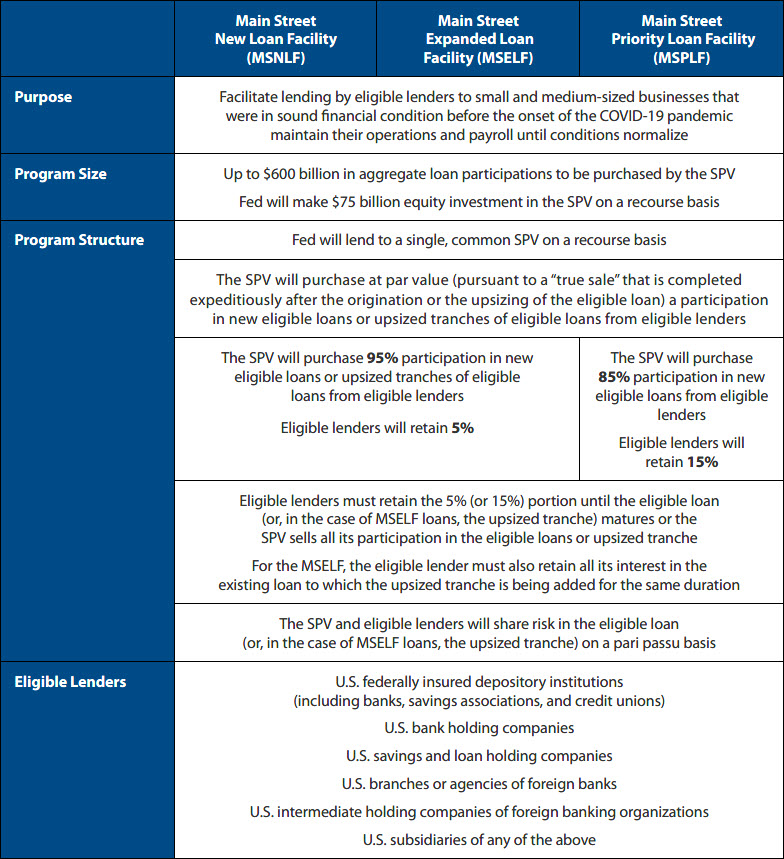

Under the Main Street New Loan Facility and the Main Street Expanded Loan Facility, eligible lenders will continue to be required to retain only a 5% share of eligible loans and will be permitted to sell a 95% loan participation to a special purpose vehicle (SPV) established by the Federal Reserve. The new Main Street Priority Loan Facility will require eligible lenders to retain a 15% share (with the SPV taking an 85% participation). The newly announced Main Street Priority Loan Facility also differs from the otherwise very similar Main Street New Loan Facility in a few key respects:

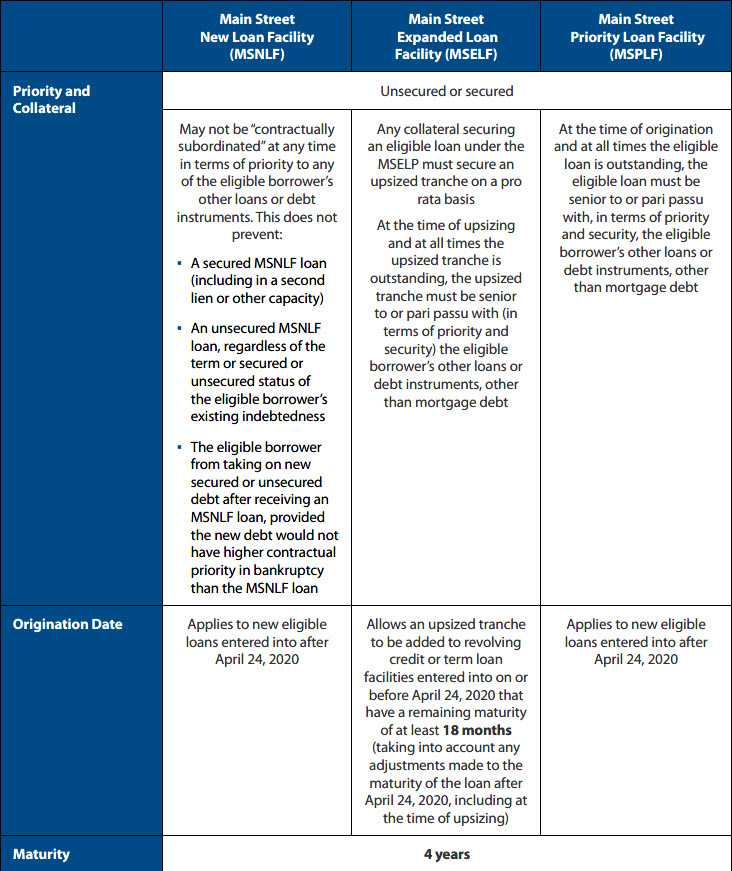

- Borrowers may borrow up to six times adjusted 2019 EBITDA rather than the four times permitted under the Main Street New Loan Facility (both up to a maximum of $25 million).

- Principal payments in years 2 through 4 are equal to 15%, 15%, and 70%1, instead of 1/3 per year under the Main Street New Loan Facility.

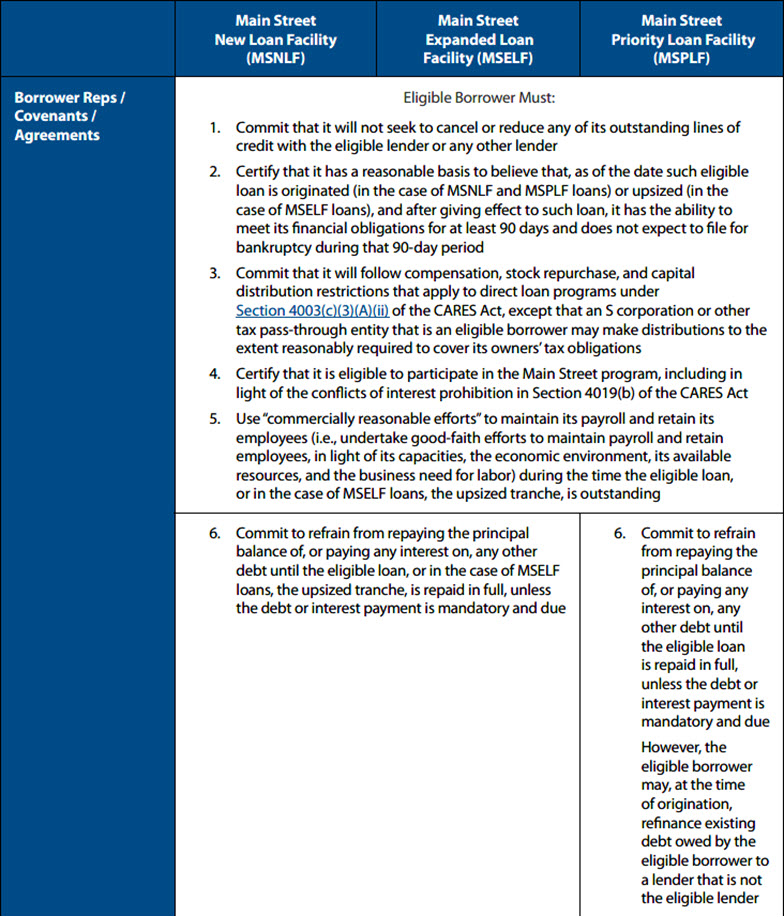

- Borrowers may, at the time of origination of a Main Street Priority Loan, refinance existing debt owed by the borrower to a lender that is not the eligible lender.

Each loan under the Main Street Lending Program continues to require an attestation from the borrower that it will comply with certain compensation, stock repurchase, and capital distribution restrictions until 12 months after the loans are no longer outstanding. While companies that have availed themselves of the benefits of SBA PPP loans remain generally eligible to borrow under the Main Street Lending Program, each eligible company will only be permitted to access one of the Main Street New Loan Facility, the Main Street Expanded Loan Facility, the Main Street Priority Loan Facility, or the Primary Market Corporate Credit Facility (a separate, $750 billion facility that will serve as a funding backstop for companies rated BBB-/Baa3 or greater).

Eligible lenders have the option to charge borrowers an attractive 100 bps origination/upsizing fee on the entirety of the additional debt, but will only retain a 5% or 15% risk retention portion, resulting in a very sizable upfront fee for underwriting and closing these loans. Lenders will also receive a 25 bps per annum servicing fee, payable by the SPV.

A summary and comparison of each Main Street Lending Program facility, including the above items, can be found below.

The Federal Reserve also released answers to Frequently Asked Questions on April 30, 2020 that provide answers to several of the questions that we raised in our first summary of the program. However, many of the original questions are yet to be answered and several new questions and ambiguities remain, including:

- How will the Main Street Lending Program be received by eligible lenders, and will the fee structure entice eligible lenders to provide adequate capital to eligible borrowers?

- Does the 5% and 15% risk retention portion of loans under the program have a chilling effect on the availability of these loans?

- Are existing lenders willing to accommodate these additional loans in existing capital structures, including in situations when the four-year maturity is inside existing credit facilities with greater maturities?

- Do upsized loans under the Main Street Expanded Loan Facility need to be incurred as an incremental loan to the existing debt and pursuant to the existing credit facility documentation, or can such upsized loans be incurred pursuant to a new loan agreement?

- Is it possible to incur an upsized loan under the Main Street Expanded Loan Facility if the existing debt is a split collateral deal with both term loans and asset-backed loans? How will borrowers satisfy the requirement that the upsized loans are “senior to or pari passu with” the existing debt of the existing lenders?

- Will the Federal Reserve open the program to nonbank financial institutions?

- Are borrowers able to certify that they have a reasonable basis to believe that they have the ability to meet their financial obligations for at least 90 days and do not expect to file for bankruptcy during that 90-day period?

- Will outstanding PPP loans be included as debt for the EBITDA/leverage limiter?

- Will media coverage of the decision of many borrowers who believed they were eligible for PPP loans to return those PPP loan proceeds discourage borrowers from applying for loans under the Main Street Lending Program, particularly given that the same affiliation rules apply?

- Will the Federal Reserve and the Treasury Department announce alternative eligibility and debt limitation metrics for asset-based borrowers and not-for-profit organizations, which are generally not evaluated on the basis of EBITDA?

Though eligible lenders can technically expect under the Main Street Lending Program to be able to sell participations in qualifying loans originated after April 24, 2020, the Federal Reserve has yet to announce when the purchase of participations will commence. Until the Federal Reserve can issue binding commitments upon which eligible lenders can rely in advancing funds, as well as greater detail on the administration of the program, it is unlikely that lenders will rush to originate these loans.

We will continue to monitor the many questions that arise and any additional guidance that becomes available.

Overview of CARES Act Main Street Lending Programs

as of April 30, 20202

Alston & Bird has formed a multidisciplinary task force to advise clients on the business and legal implications of the coronavirus (COVID-19). You can view all our work on the coronavirus across industries and subscribe to our future webinars and advisories.

1 The Main Street Expanded Loan Facility also provides for the 15%, 15%, and 70% amortization structure.

2 Summaries are based on term sheets published by the Fed on April 30, 2020.

3 Fed defines a business as an entity that is organized for profit as a partnership; a limited liability company; a corporation; an association; a trust; a cooperative; a joint venture with no more than 49% participation by foreign business entities; or a tribal business concern as defined in 15 U.S.C. §657a(b)(2)(C), except that “small business concern” in that paragraph should be replaced with “business” as defined here. Other forms of organization may be considered for inclusion as a business under the Main Street Lending Programs at the discretion of the Fed.

4 To determine how many employees a business has, it should follow the framework set out in the SBA’s regulation at 13 CFR 121.106. As set out in 13 CFR 121.106, the business should count as employees all full-time, part-time, seasonal, or otherwise-employed persons, excluding volunteers and independent contractors. Businesses should count their own employees and those employed by their affiliates. In order to determine the applicable number of employees, businesses should use the average of the total number of persons employed by the eligible borrower and its affiliates for each pay period over the 12 months before the origination or upsizing of the Main Street loan.