On February 10, 2022, the U.S. Securities and Exchange Commission (SEC) proposed amendments to the rules governing beneficial ownership reporting under the Securities Exchange Act of 1934 Sections 13(d) and 13(g). The amendments are intended to modernize Schedule 13D and 13G filings by addressing “information asymmetries” and the timeliness of filings.

Schedule 13D and 13G Filing Deadlines

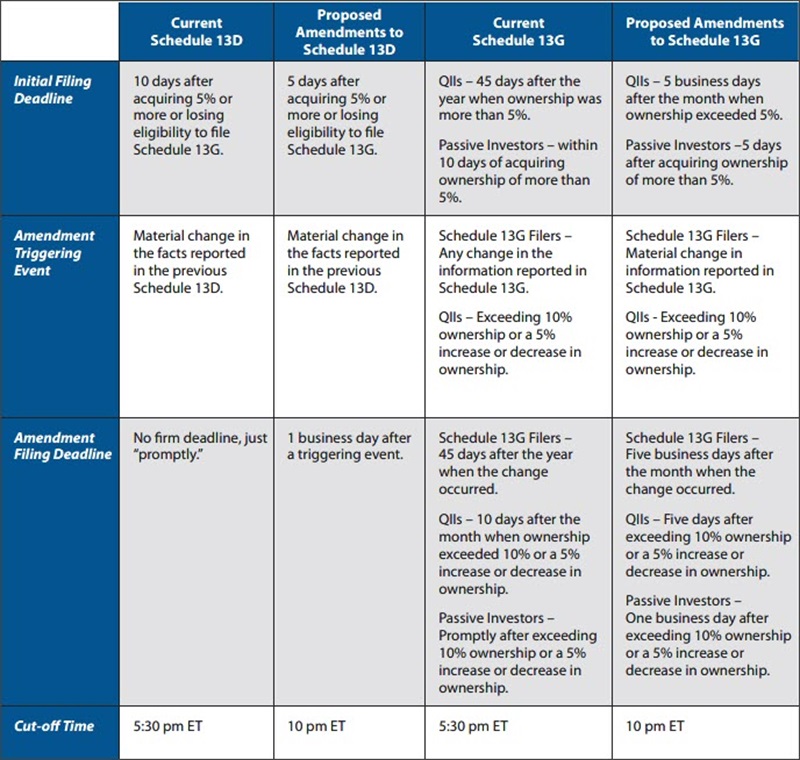

The Dodd–Frank Act amended Section 13(d)(1) to give the SEC the authority to shorten the filing deadline for the initial Schedule 13D or Schedule 13G, but the SEC has not implemented a shortened deadline. With the rising use of electronic filings, there has been a call by issuers to shorten the filing deadline to meet the needs of today’s market and ensure that material information about change of control transactions is released to the public in a timely fashion. The SEC believes that the current rules do not meet the needs of investors and proposes to use the power granted by the Dodd–Frank Act to shorten the deadline.

Proposed Schedule 13D filing deadlines

Under the current rules, a holder must file a Schedule 13D within 10 days after an acquisition of more than 5% of registered voting equity securities and must “promptly” thereafter file an amendment to report any material changes. The SEC has proposed shortening the 10-day deadline for the initial filing to five days and believes that the proposed five-day deadline strikes a balance between the needs of issuers of securities and large shareholders. The SEC is also proposing that any amendments to a Schedule 13D must be filed one business day after the triggering event.

Proposed Schedule 13G filing deadlines

Additionally, the SEC proposed amendments to shorten the deadlines for initial and amended filings by beneficial owners who are eligible to file a Schedule 13G. Currently, beneficial owners can file the short-form Schedule 13G if they are a passive investor – investors that do not intend to change or influence control of the business or have another disqualifying purpose or effect.

The current deadlines for filing a Schedule 13G depend on whether the beneficial owner files as a qualified institutional investor (QII) (pursuant to Rule 13d-1(b)), a passive investor (pursuant to Rule 13d-1(c)), or an exempt investor (pursuant to Rule 13d-1(d)).

To help filers adjust to the proposed filing deadlines, the SEC is proposing to extend the cut-off time for filing any Schedule 13D or 13G with the SEC from 5:30 pm ET to 10 pm ET, similar to the current filing window available for Section 16 filings. (see table below)

Disclosure of Cash-Settled Derivative Securities

The current rules only require physically settled derivates to be included in beneficial ownership calculations and disclosed if they can be settled within 60 days. The current rules do not require cash-settled derivatives to be included in the holder’s beneficial ownership of the reference security. The SEC is concerned that a person may acquire or hold cash-settled derivatives and use their position to influence the counterparty’s voting, acquisition, or disposition of shares acquired in a hedge or proprietary investment.

Under the proposed amendments, holders of certain cash-settled derivative securities will be treated as beneficial owners of the reference equity securities if the securities are held with the purpose or effect of changing or influencing the control of the issuer.

Group Formation and Exemptions

The SEC is proposing a series of amendments to Rule 13d-5 to clarify its position that the formation of a “group” under Sections 13(d)(3) and 13(g)(3) and Rule 13d-5 of the Exchange Act does not require the existence of an agreement (express or implied) between the parties to act together for the purpose of acquiring, holding, voting, or disposing of the securities. The SEC provides an exhaustive discussion of the legislative history for its conclusion that merely acting together for the purpose of acquiring, holding, voting, or disposing of shares is sufficient to form a group for Sections 13(d) and 13(g) purposes.

As part of the SEC’s clarification of the legislative history of Sections 13(d) and 13(g) groups, the SEC is proposing a new rule to affirm that if a person who is required to file a Schedule 13D discloses to any other person that such filing will be made and the other person acquires any subject securities, then those persons have formed a group for Section 13(d) purposes.

Additionally, the SEC is proposing exemptions from the group requirements under Sections 13(d)(3) and 13(g)(3). Under the proposed exemptions, a group would not be created when shareholders engage with other shareholders and the issuer on matters that are not undertaken with the purpose or effect of changing or influencing control of the issuer (e.g., a nonbinding shareholder proposal). Also, a group would not be created by persons who enter into a bona fide derivative security agreement in the ordinary course of business and not for the purpose or effect of changing or influencing control of the issuer.

Structured Data Requirements

Lastly, the SEC is proposing to replace the current requirements for Schedule 13D and 13G filings on EDGAR with a Schedule 13D/G-specific XML. Reporting persons would be able to file directly with EDGAR or use a web-based application for their filings.

Additional Actions

Comments from the public are due on or before 30 days after publication of the proposals in the Federal Register or April 11, 2022, whichever is later.